Retirement Planning Calculator

Calvin Lim · RNF: CLK300309940 · PromiseLand Financial Advisory Pte Ltd

Retirement Gap Calculator

Discover how much your CPF LIFE will cover — and how Calvin's plans can close the gap. Income target is entered in today's dollars; 2% annual inflation is applied to show the true future cost.

Inflation disclaimer: Monthly income target is expressed in today's dollars (2026). A 2% annual inflation rate is applied over the years from today to the desired retirement year. The 2% rate is based on Singapore's long-run core inflation target and is for illustrative purposes only. Actual inflation may differ. CPF LIFE payouts shown are nominal and not inflation-adjusted. Members on the CPF LIFE Escalating Plan receive payouts increasing at 2% p.a., which partially hedges against inflation.

Product disclaimer: Dividend payout of 6% p.a. is non-guaranteed. Manulife IncomeGen (II) illustrated payout of 3.24% p.a. of total premiums is based on a 4.25% p.a. participating fund return and is non-guaranteed; guaranteed income is 0.81% of total premiums p.a. Figures shown are the nearest available premium tier ($50k, $100k or $150k annual premium) sufficient to cover the gap. Past performance is not indicative of future results. All figures are for illustration purposes and do not constitute financial advice. Please consult a licensed financial adviser before making any financial decisions. Calvin Lim Kian Seng · RNF: CLK300309940 · PromiseLand Financial Advisory Pte Ltd · Licensed by MAS under the Financial Advisers Act. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Plan Illustrations

Explore detailed projections for each plan, then compare them side by side.

Option 1 — Dividend Payout

Pay annually for 3 years. Receive monthly dividend payouts for life. Dividends are 6% p.a. of the fund value each year.

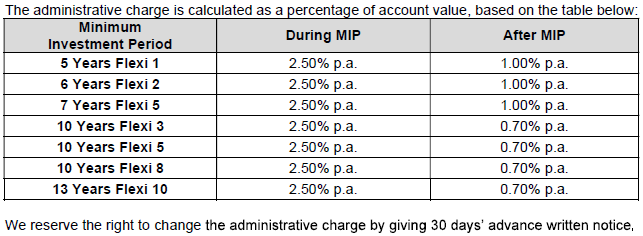

Offsetting the 0.7% gross charge → net 0.4% effective drag

2.5% p.a. gross charge, no loyalty bonus yet

0.7% gross charge − 0.3% loyalty = 0.4% net p.a.

0.7% gross charge − 0.3% loyalty = 0.4% net p.a.

Option 2 — Manulife IncomeGen (II)

Pay annually for 3 years. Monthly income begins from the 49th monthiversary (~4 years after policy start). Capital is fully preserved from year 5 onwards. Participating whole life plan — payout comprises guaranteed and non-guaranteed components.

0.81% of total premium p.a. ÷ 12

= 3.24% × total premiums ÷ 12

= 3.24% of total premiums p.a.

Higher of 101% total premiums OR sum insured

Capital fully preserved from yr 5 onward

Capital + non-guaranteed surplus bonus

Capital fully preserved throughout

Compare both options

Adjust sliders in each tab, then return here to compare.

Dividend Payout

Manulife IncomeGen (II)

*Disclaimer: Figures for illustrative purposes only (Please refer to T&C for further information) Please click here for T&C* if required

IN DEPTH FINANCIAL PLANNING

Our Advisory Work With Your Financial And Life Priorities To Develop A Comprehensive Strategy

PLANNING AHEAD

Plan Your Retirement With The Help Of Our Holistic Investments

CUSTOMISED PORTFOLIOS

Get Access To Bespoke Portfolio Solutions, Choose From Various Investment Themes

Thematic

Gain Access To Current Trends

Geographical

Explore Yourself To Different Countries And Regions

Sector

Access Sectors Specific Funds And Investments

Income

Invest Into Investment-Grade Fixed Income Securities And Bonds

ACCESS TO NON RETAIL INVESTMENTS

Invest In Institutional And Accredited Investor Only Offerings

TOP PROFESSIONAL QUALITY SERVICE

Insurance Brokers Singapore Financial Adviser Representatives Are Yearly Million Dollar Round Table (MDRT) Awardees With Multiple Other Accolades Including Yearly Insurance And Investment Achiever Qualifiers.

HELPING YOU FIND THE BEST PLAN

In The Market With Our Trusted Insurance And Investment Partners.

Calvin Lim Kian Seng

RNF License Number: CLK300309940

Promiseland Financial Advisory Pte Ltd

Mobile Number: (+65) 9510 4676Email: calvin.lim@promiseland.com.sgIndustry Accolades: MDRT 2021, 2022, 2023, 2024, 2025, 2026, 2027

Insurance Brokers Singapore is a privately owned website operated by Calvin Lim Kian Seng, a Financial Adviser Representative of PromiseLand Financial Advisory Pte Ltd, a licensed Financial Adviser under the Financial Advisers Act (Cap. 110) and regulated by the Monetary Authority of Singapore (MAS). As an appointed Financial Adviser Representative of Promiseland Financial Advisory Pte Ltd, Calvin is authorised to provide advice and to arrange the following types of products:

- Health Insurance

- Life Insurance

- Investment Linked Policies (ILP)

- Collective Invest Scheme (Unit Trust)

Throughout his journey, he has assisted many families in their financial planning, and helped them handle insurance claims.